Bear Market Over or Beginning?

Bear Market Over or Beginning?

Will Powell stick to his lesson or get cold feet?

Source: S&P Global Flash US Composite PMI, Demand weakness weighs further on private sector business activity in November

The market rallied on this news because investors still can’t believe the Federal Reserve will fight inflation. They think it will fold at the first sign of weakness.

In the next bit from the linked report above, he mentions the trouble finding skilled workers. When will this canard go away? Probably in the recession.

How do I know it is a canard? History tells me. It’s amazing how few economists go back and read what the Federal Reserve was writing in 1973 during the oil shock and high inflation:

The expansion in economic activity has slowed in recent months, but inflationary pressures have remained extremely severe. In view of the persistent buildup in the backlog of unfilled orders, continued pressures on capacity, and rather widespread shortages of materials and skilled labor, much of the slackening in real growth probably reflects supply limitations.

I pulled a bunch of these during the summer: Economic Highlights of 1973. It didn’t take me long because this story was repeated throughout as it is in today’s financial media.

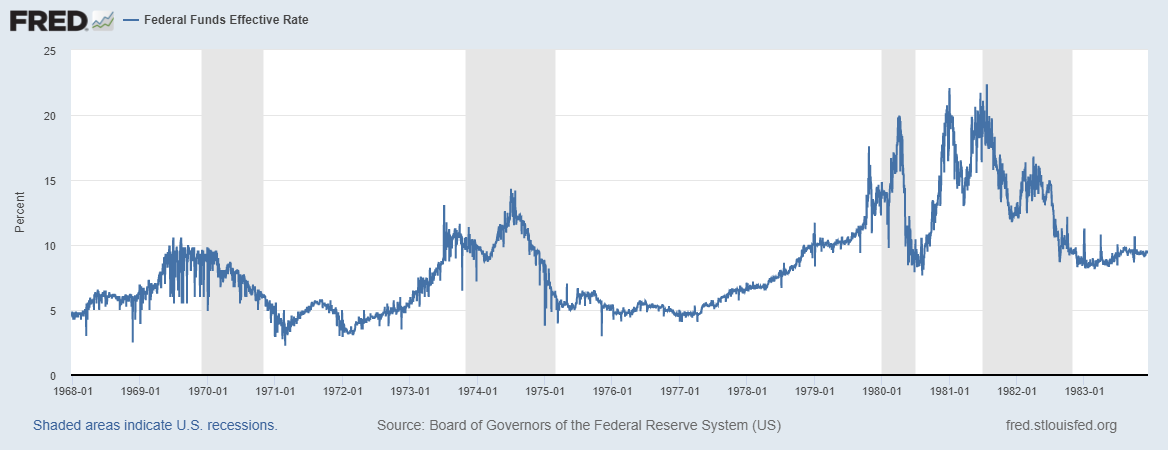

Back in August, current Federal Reserve Chairman Jerome Powell said he learned the lessons of the 1970s. If you’re unfamiliar with the history, here it is in a chart of the Federal funds rates. The gray boxes are recessions.

See how the Fed cut rates in the recession? The result was higher inflation followed by higher interest rates until it became so bad that people thought the U.S. dollar might collapse. Then Chairman Volcker helped trigger the worst recession since the 1930s by hiking the Fed funds rate up to 20 percent.

Going back to Powell. In August 2022 he spoke about the lessons:

"Restoring price stability will likely require maintaining a restrictive policy stance for some time," Powell said. "The historical record cautions strongly against prematurely loosening policy."

Powell said that bringing inflation down will require "a sustained period of below-trend growth" for the U.S. economy. He acknowledged that Fed policy tightening will bring "some pain to households and businesses." But "far greater pain" would result from a failure to restore price stability.

Powell is talking about the above chart. He understands the option is a recession now or a bigger one later. Whether he can hold the line with the clowns of the FOMC, who knows. These morons were pumping QE well into 2022 with inflation running towards double-digits. Powell seems to have had the fear of God put into him, but a growing number of the others are jellyfish who serve their political masters. The current leaders of the Globalist American Empire (GAE) are into Modern Monetary Theory aka “we can make money printer go brrrrr and it won’t cause inflation.”

I have no certainty about policy because Federal Reserve officials do policy 180s all the time. All I can say is that Powell has spoken in a way that tells me that 180-degree turn might be much later than expected by the market.

In conclusion, the bull case for stocks: the Fed folds and cuts interest rates. Stocks will rip to all time highs, crypto will be saved, the poor and middle class will be crushed into dust.

The bear case for stocks: the Federal Reserve will not cut interest rates at the first sign of deflation because Powell knows the CPI will probably hit double-digits if he does. When bulls are being slaughtered on Wall Streets and the gutters overflowing with their blood, they will look to Powell to save them. “Please Chairman Powell, cut the interest rates.” And Powell will look down at them and say, “No.”