East Asian Currencies at the Krakatoa Line

East Asian Currencies at the Krakatoa Line

The East sees hawks, not doves, from the FOMC

First a quick note on BTC. Could be a trip down to the $50,000 area if support around $60,000 is lost.

On to East Asia.

Two cycles are coinciding: a global stock market bull and a U.S. dollar bull. The prior two shifts from U.S. dollar to foreign leadership and vice versa, occurred during the prior two bear markets in 2000 and 2008.

The S&P 500 Index is up more than 350 percent from the 2008 top. Measured by relative stock prices, foreign stocks appear overdue for outperformance versus U.S. stocks.

Currency charts suggest that the first move could be a nominal decline in foreign and U.S. stocks should the U.S. dollar slip the surly bonds of final resistance.

South Korea, Japan and China

East Asia combines for around 27 percent of global GDP. The United States accounts for about 28 percent, all as of 2023.

In U.S. dollar terms via the South Korea ETF, we see a fund with a 16 percent total return since 2007.

The Nikkei in USD or JPY has been dead money since 1989. This is not relevant measure for the cycle though. The Nikkei is up 80 percent is USD and 125 percent in JPY from the 2007 top.

The Shanghai Composite is up about 50 percent in USD since the early 2000s. That’s better than in CNY which has appreciated since then.

East Asian Currencies

Here’s a basket I made of these, similar to the ADXY:

The U.S. crosses on all these currencies are all at or near final resistance levels. The next move will be explosive rallies if they take out that resistance. JPY will trade at multi-decade lows, CNY at a 17-year low with very little chart resistance. KRW is the strongest of the bunch in terms of the short-term chart position. USD has to rally less than 1 percent, less than 2 percent and less than 8 percent against JPY, CNY and KRW to achieve a breakout. That said, the long-term chart of KRW shows it has only spiked above the current level, therefore I suspect if there’s turmoil, that 7 percent distance will close fairly quickly.

Assessing the Risk

My experience with these situations is they usually do not follow through at scale. This isn’t a $50 billion market cap company. Fortunes can change overnight for firms, be it perception or reality. A run from $50 billion to $100 or $25 billion is huge for the firm and their shareholders, but a drop in the financial ocean.

Not so East Asia, and since the U.S. dollar is on the other side of these crosses, we’re talking about more than 50 percent of the global economy. Major technical events in either direction are indicative of extant or pending trend changes and or powerful events.

It’s also the case however, that prior peaks are associated with acute stress in the markets. Either commodity sell-offs and weakness in China, or both, or bear market moves in global assets.

Today, there is very little stress evident in the equity markets. The Federal Reserve made a dovish pivot last year and Powell confirmed that pivot with his press conference. Markets immediately interpreted it dovishly, though they have been backing off that move.

A breakout in the dollar vs East Asian currencies would therefore be both acutely counter-trend to the global markets (not to their own charts though) and at the same time would occur quietly considering the implications. A major rally in the U.S. dollar versus East Asian currencies screams financial crisis in China or global recession, or both.

Point being, investors and traders alike paying attention here can establish related short position at relatively cheap cost because the equity markets are acting as if there’s no chance of a USD breakout.

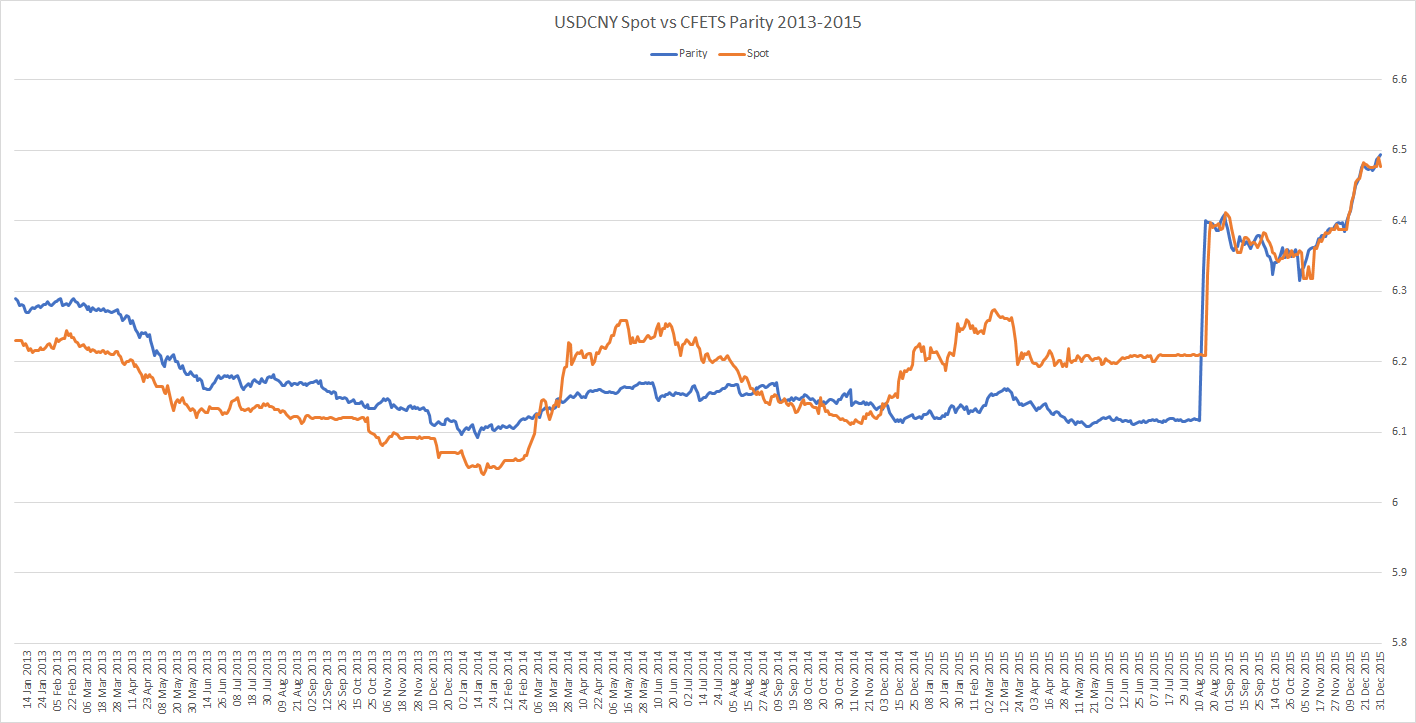

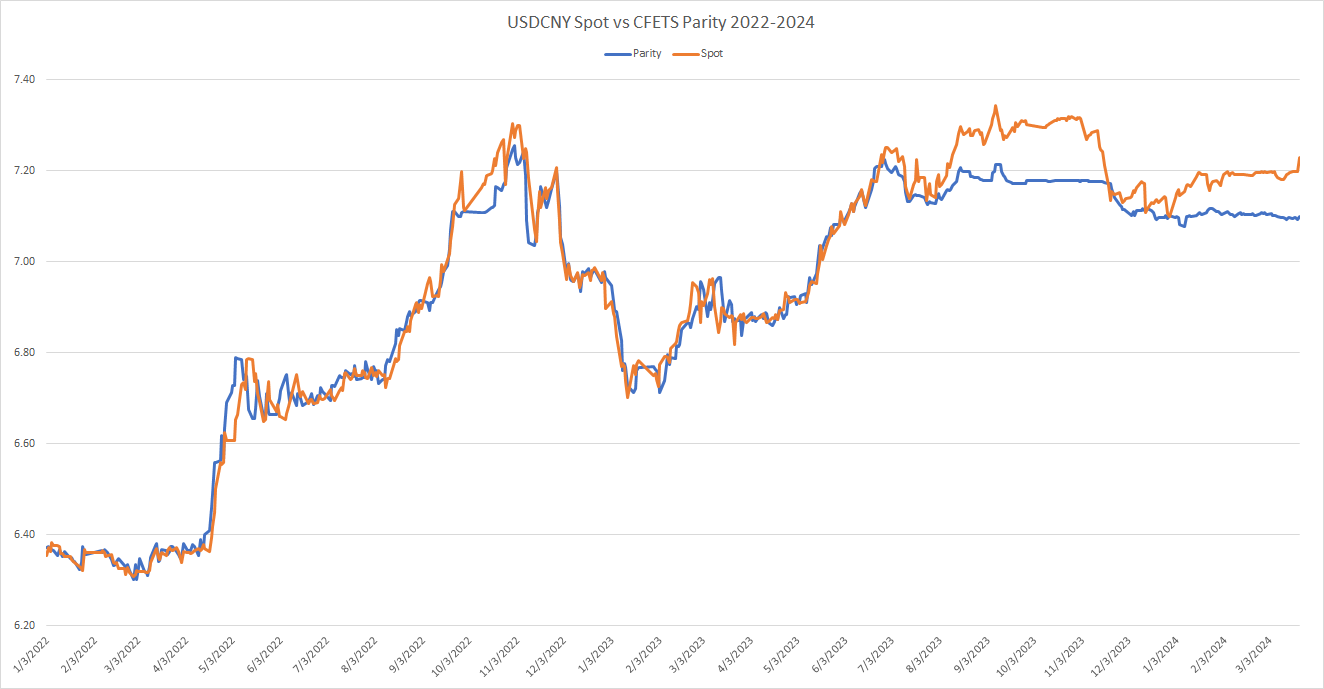

Final chart. Here’s a comparison of the Chinese exchange rate in orange versus the central parity rate set by the government in blue. First is the leadup to the 2015 depreciation and second is now.

Both periods saw first a breakout in USDCNY away from parity, then a fall back, followed by another break. There was intervention both times on the second break, evidenced by the nearly flat line in the exchange rate. China moved the parity rate up today after USDCNY popped.

iFeng: 外汇市场异动,离岸人民币汇率突破7.27关口,什么情况?

Quoting a Soochow Securities macroeconomist, machine translated:

First of all, the macroeconomic background is mainly the strength of the US dollar and the weakness of the Japanese yen. The strength of the US dollar is self-evident. Although the Federal Reserve's interest rate meeting this week maintained the guidance of three interest rate cuts this year, from the perspective of the foreign exchange market, this is more hawkish than expected. In addition, the Swiss National Bank took the lead in cutting interest rates, and the Bank of England was obviously dovish, so the strength of the US dollar is reasonable.

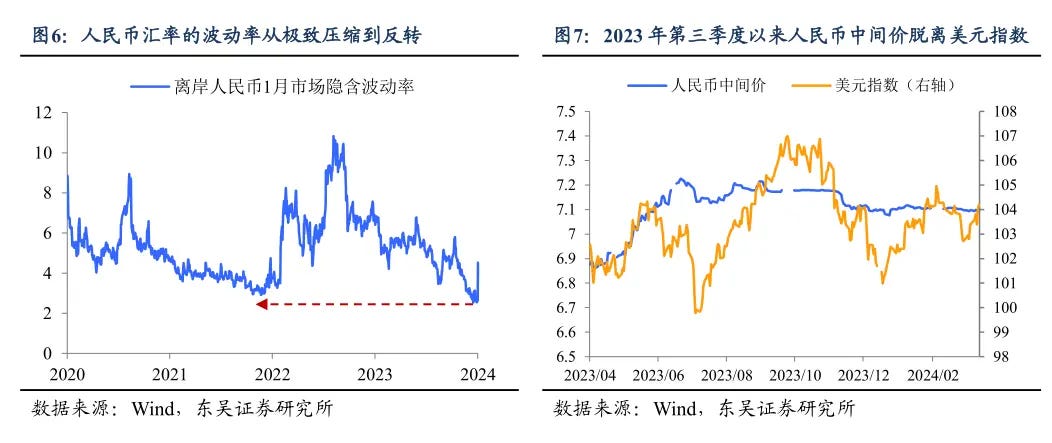

Secondly, from a policy perspective, 7.20 is not a hard constraint. What indicator best represents the central bank's exchange rate view? That is the central parity rate. Since February this year, the central bank has basically maintained the central parity rate at around 7.10. According to the official exchange rate system, 7.24 is the real lower limit of the onshore RMB, while 7.20 is more like a tacit understanding of the market.

The third is the characteristics of the market situation. The volatility of the RMB exchange rate is relatively low. The volatility of all assets will follow the law of movement when things reach their extremes (in the absence of structural changes in the market). Due to the constraints and tacit understanding of stabilizing the exchange rate, the volatility of the RMB exchange rate hit the lowest value since the epidemic in March this year, even lower than March 2022. After March 2022, due to the epidemic, the RMB exchange rate once fluctuated sharply, adjusting from 6.3 to 7.3.

What is the role of accidental events? "Assembly call". The draft of the US's restriction on investment in China, which was released overnight, plays more of a role of "breaking the cup as a signal", giving the market a signal of unifying steps and moving towards inevitability in the short term when no one is willing to take the first step.

The chart on the left shows CNY volatility, the right is central parity vs DXY.

Summing up the article’s main revelation: the market was sitting at a breakout point that no one wanted to breach, then the U.S. investment regulation draft triggered a move.

What happens if the 152 level of USDJPY, considered the level at which the Japanese authorities intervenes, falls? A major breakout in USD could rapidly unfold.

What if the 152 level holds and East Asian currencies rally? The immediate implication is bullish for global markets, but mainly because a bullet was dodged.

The move could be a temporary pullback before a breakout in USD later this year or it could mark a significant top for the dollar. Unlike a breakout however, it will take some time before the charts indicate a more serious breakdown is underway, though there could evidence from other markets providing corroborating evidence. A coincident breakout in a relevant commodity such as copper or strong upturn in trade and economic data in East Asia for example.

How to Trade Both Scenarios

I don’t own a crystal ball so context can change, but right now I expect a U.S. dollar breakout will initiate a violent culmination of the 15-year bull market in U.S. equities. I expect SPY will underperform EFA and EEM in the move, but perhaps not currency adjusted. This will be the tell for a leadership transition, and it will also be evident by U.S. tech sectors leading the U.S. market lower. I want to be short U.S. tech on the way down and long emerging market commodities on the way up (coal, copper and so on).

In a dollar breakout, I’m looking for bearish trades on U.S. equities, targeting the most overvalued sectors. Long vol, high-risk, high-profit, higher-frequency shorter-term trades rolling profits into dollar bear trades. Some commodities probably bottomed already, as oil did in 1998 ahead of the 2000 bear market, but they will go lower from here in a recession.

In a dollar breakdown scenario, I’m looking for bullish trades on foreign equities, emerging markets, with a special focus on natural resource producers and commodities. I will make investments with an expected holding period of 5 to 10 years.

To a degree, this is all one scenario. The U.S. markets are at a relative peak versus most foreign markets (driven by relative weights in technology), relative valuations between assets such as tech and commodities are at similar extremes. Even within asset classes, gold miners versus gold for instance, speak to peaking pessimism. It’s possible currency moves are so extreme that investors in e.g. China, panic into stocks.

The difference in these scenarios is timing and confidence. If the dollar soars in a global bear market and recession, I will have high confidence in buying lows in commodities and foreign markets. If instead the turn is underway and the bull is already running, there’s still plenty of time to get in, but for the rest of 2024 and into 2025 will be a lingering concern (assuming economic data doesn’t clarify) that a major bear market is still ahead, in which case cheaper entries in the long trades will be possible.