The Based Take on China's RRR Cut

I’m going to cover the RRR cut below if you want to cut to the chase. First an interlude about what it means to be based.

Based refers to people and ideas. A based person confidently speaks truth without regard for the consequences. It’s about being yourself and ignoring the crowd. When talking more about ideas, it refers to speaking truthfully. There’s a sliding scale according to a person’s status in society.

In charting, a basing pattern is a consolidation phase. It can be large with substantial price moves, but ultimately it forms something like a U-pattern. The cup-and-handle is a specific basing pattern.

In a nutshell, a base is a long period of changing ownership of a stock. Holders sell to new buyers who have a lower average cost of ownership. Eventually the selling dries up as everyone who wants out is gone. When the stock starts climbing out of the base, a new source of buyers come into a market where few of the holders want to sell.

The opposite is a top. The buyers dry up as everyone who wants to buy has bought in. As the stock starts to drop out of the base, new buyers are overwhelmed by holders who want out.

When I noticed networking stocks were gaining momentum, I went through the charts and found Extreme Networks (EXTR) as my favorite. I posted it here on October 31 when the price was $17.94. It hit $19.92 on Wednesday, a gain of 11 percent. What’s different about this chart is that it is outright bullish. This isn’t a rebound in wrecked stock; it has broken out of its 20-year base. I wouldn’t buy here unless I was overall bullish on the market because bullish patterns often fail in bear markets, but if this isn’t a bear market, I think this could be a big winner.

Basing can also happen at the top. Here’s my chart of Tesla turned upside down:

BasedMoney is focused on finding BasedCharts with great profit potential on the bullish or bearish side, along with based takes on the markets and economy. One such take I posted this morning, on the much-hyped diesel shortage.

Now it’s time for the China reserve-ratio-requirement cut (RRR).

The RRR is the amount of cash reserves banks must hold. When it goes up, banks must add capital before lending. When it goes down, banks can lend more against their existing reserves.

Whenever the RRR is cut, there will be articles claiming this is bullish, that it releases liquidity. In theory it does, but in practice, China cuts the RRR when its banking system is under stress. Banks can lend more, but they often don’t.

Another point: the earnings per share of emerging market companies is positively correlated with the Chinese 10-year yield. The performance of emerging market stocks is also positively correlated with both the 10-year yield and the RRR rate.

Here’s the evidence of the emerging market stock performance versus the RRR. This is the iShares MSCI Emerging Market ETF (EEM) divided by the SPDR S&P 500 ETF (SPY) in orange. A falling line indicates EEM underperforming. The RRR is in blue. Today’s cut is not on the chart yet. It was cut to 11 percent.

In the past the relationship wasn’t as tight. I expect the EEM/SPY ratio will turn higher before the RRR cut goes higher. When a divergence develops, that’ll be evidence of a trend change.

Here is the Chinese 10-year government bond yield versus the EEM/SPY ratio in orange.

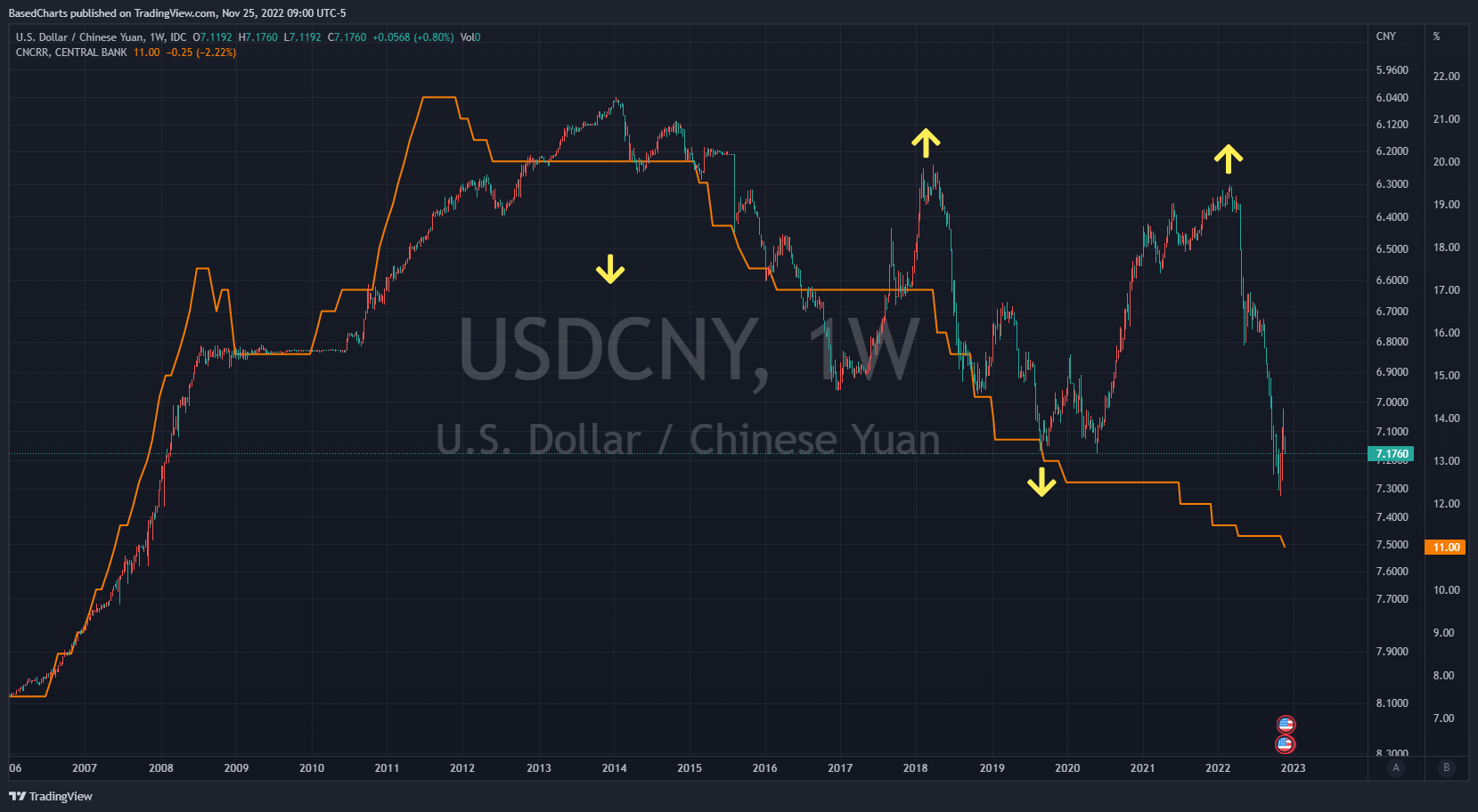

How about the Chinese currency? This chart shows the RRR in orange against the Chinese yuan, here shown as the USDCNY exchange rate inverted. (Ignore the arrows, they did not invert.)

The RRR becomes less predictive over time, but there is still a relationship. The yuan falls soon after RRR cuts in 2015 and 2018. The yuan typically rallies after the RRR is left unchanged for a long period. Perhaps this will be an outlier like in 2020 when the RRR was cut, but the yuan didn’t make a new low. Until I see otherwise, I expect a new low for the yuan, and a new high in USDCNY is ahead.

Finally, there’s China’s credit system. Since 2008, China has seen slowing growth. Every effort at boosting credit triggered another expansion in the housing bubble. In 2017, Xi Jinping said “houses are for living in, not speculating on.” Result: credit growth slowed. China hasn’t reformed its domestic economy, instead moving in the opposite direction with tighter state control. Debt-financed infrastructure spending leads to slower growth. They don’t want unsustainable expansion in the credit or housing bubbles. The RRR cut is most likely in response to tight liquidity conditions. They are taking pressure off the banks, but they are not alleviating the pressure. Unless and until the trend changes, evidence by emerging market stocks outperforming U.S. stocks, the U.S. dollar falling, GDP slowing and so on, more RRR cuts will follow.

If you enjoyed this post, please consider subscribing or sharing this post with others.