The Case for a Market Top

Well, yesterday’s stagflationary GDP report didn’t shock the market. After backing out the move in Meta, the market was barely down on the day. It was, overall, a big win for the bulls. I closed out my weekly Crazy Trades expiring on Friday with a net gain, but shrunk by the fact that Nvidia-buying bulls pushed SMH higher. Re: that post, I am sticking with XLC for now as explained below, still have TSLA and will keep adding XLV as appropriate.

My hunch is yesterday’s bullish counterattack it will go down as something more like the Battle of the Bulge.

The 2s10s remains in a symmetric pattern. The structure is busted, but the time symmetry hasn’t yet. It fell below zero in July 2022. It bottomed in July 2023. A year later would be July 2024. There’s still about 12 weeks until the pattern’s time symmetry falls apart. I don’t place a great deal of strength on the time aspect, rather the massive basing pattern and inevitable steepening that will come at some point.

Bears as a group mostly focus on index trades, specifically the major indexes. Or major stocks like Apple and Tesla. At several points, I have recalled wondering what bears are complaining about because other markets were already deteriorating. Back in the summer of 2018 (when I started dipping my toe into actively trading in bear markets), emerging markets had already weakened. Crypto, emerging markets and the ARKK-led speculative complex all topped in February 2021 when long-term yields started rising.

What’s weakening now? Well first off there is the possible top already formed in the major market indexes. This isn’t a robust top, but right now it could be.

I mentioned XLC above. Google manipulated its stock higher in after hours with a buyback and dividend, aka their actual story is not good. At the moment, the spike in Google isn’t enough to close the gap on XLC, but even a successful gap fill wouldn’t negate the double top. Google alone is a scary looking chart for bears, but I think XLC tells the real story. I’ll grow my position at a gap fill.

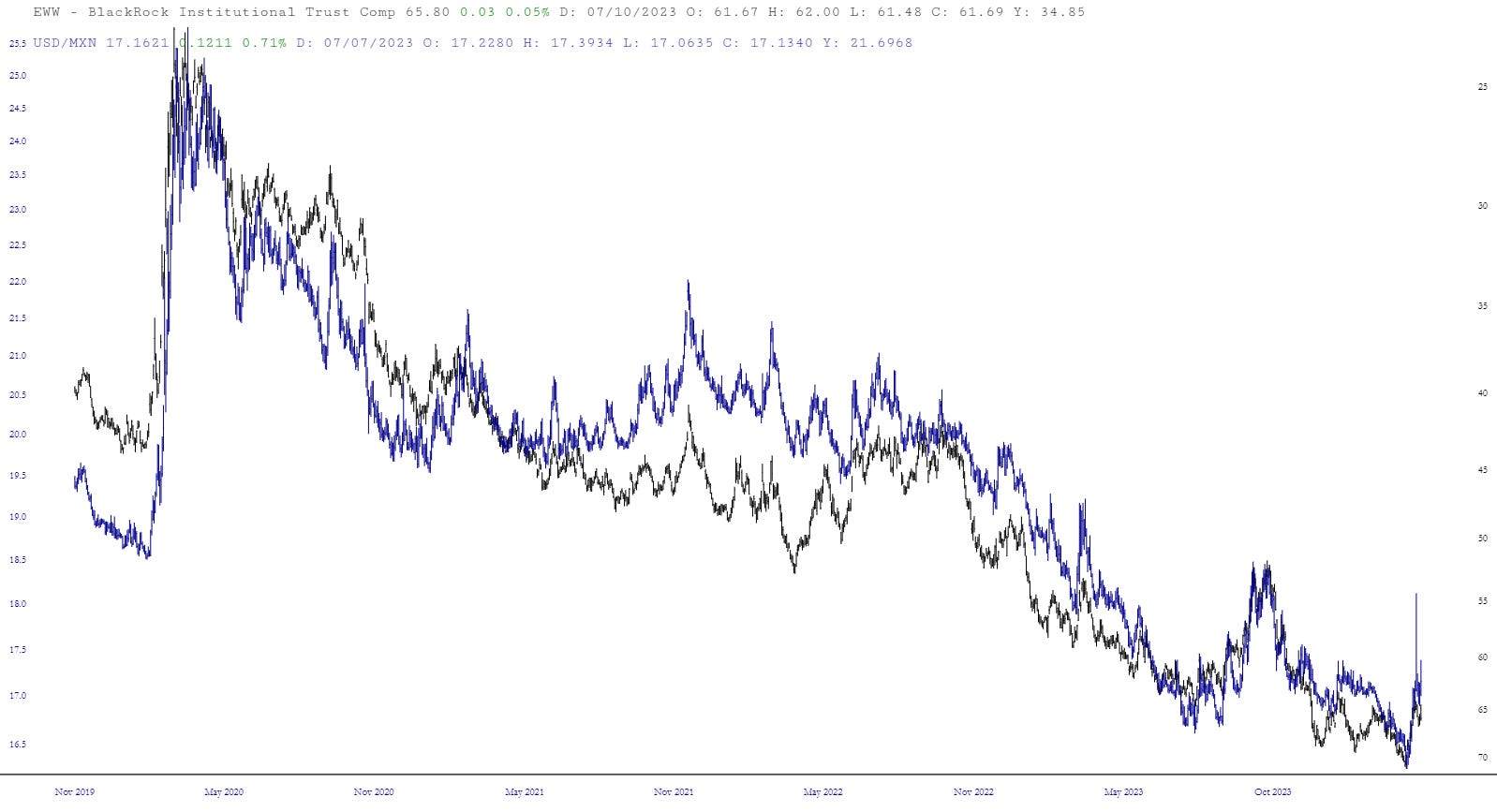

How about emerging markets? I often post USDMXN as a VIX-whisperer. If I’m correct that it has reversed, EWW 0.00%↑ has topped.

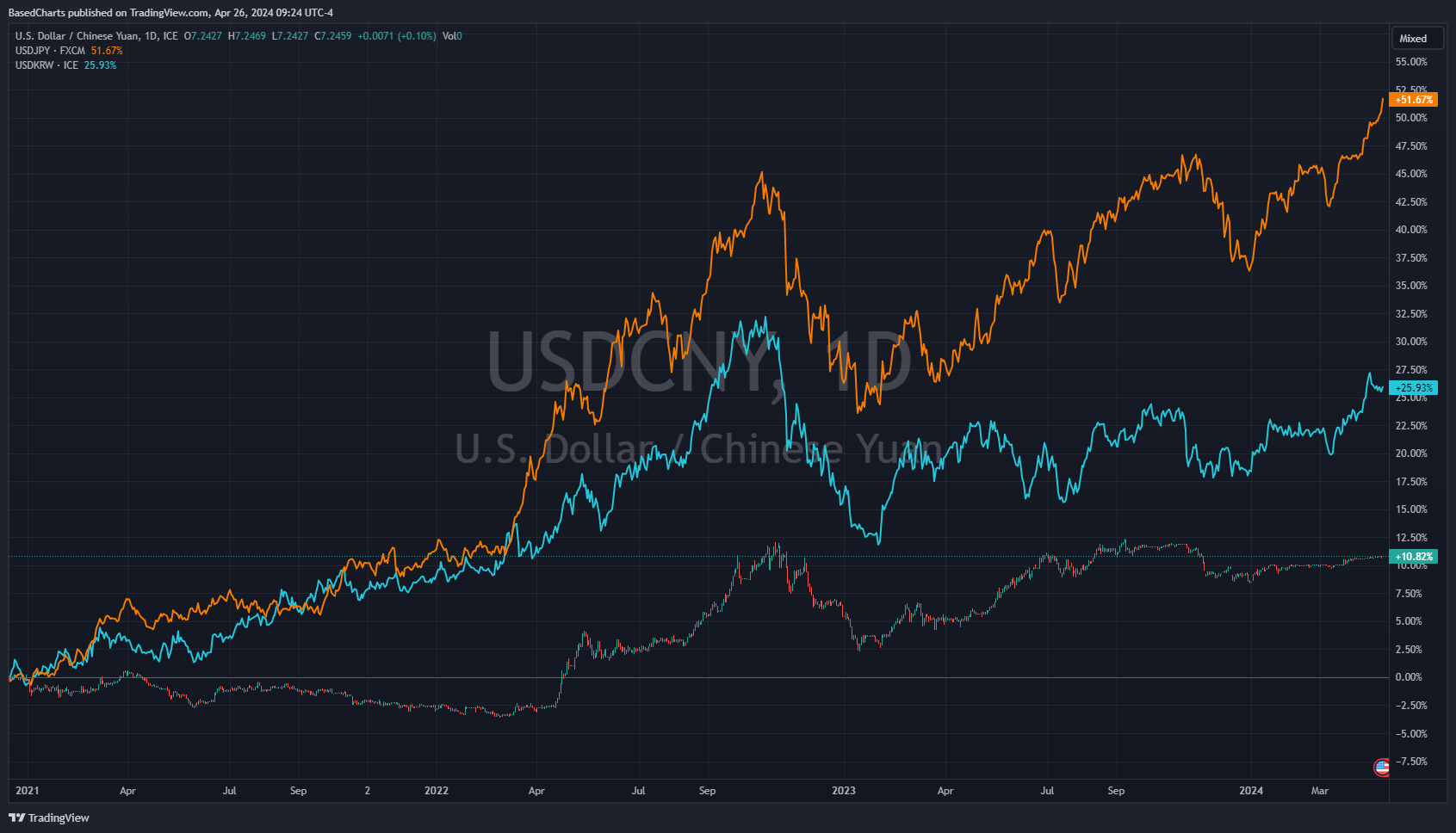

The yen tanked today after the Bank of Japan held off on rate hikes. As a bloc, East Asian currencies are now below the 2022 low. USDCNY is pinned at the top of its trading range as China tries to keep the yuan from following.

There are two ways to look at commodities such as copper and oil here, but neither interpretation is particularly favorable for stocks.

The rising U.S. dollar is sucking liquidity out of global central banks:

If the dollar cannot provide liquidity, the alternative is local currency. Increase the supply of local currencies much faster and what happens to USD?

Unstable Equilibrium

The market is pinned in a state where lower bond yields send inflation higher via commodity rallies, and then rates go back up. The 2s10s reflects this state of affairs. It cannot steepen because the Federal Reserve sees no need for cuts yet, or at least cannot justify them. On the other side, the long-end of the curve will not break out because the market doesn’t see inflation taking off from here. As long as the curve is inverting or pinned in an inverted state, the stock market can rise.

The recent steepening produced the March top though. When the curve is done fooling around with inversion, the bull market will be over in hindsight, because the market goes down whenever the trend is towards steepening.

It’s a frustratingly long process, but nothing has stopped the trend. Moreover, the bullish spurt from October 2023 to March was initially supported by moves in bonds, the U.S. dollar, consumer price inflation and so on. They are all reversing now or have already reversed the entirety of their moves back to those October 2023 levels.

Inflation Always Ends

Inflation sprays money into an economy and it does not all go into the pockets of those who produce value. It goes into the pockets of people who are politically connected or who happen to own assets that benefit from the inflation, along with value producers. It doesn’t go into the pockets of prudent investors, it goes into the pockets of the most aggressive speculators who behave as if inflation will never end.

Inflation is a destructive process whereby economic activity shifts into unsustainable activities that exist because of said inflation. The longer the inflation, the greater the inevitable bust.

Many, myself included, who see the inflation have a hunch that inflation will continue and therefore assets such as copper will rise in the long-run, but even that is not confirmed yet because it requires subsequent rounds of inflation. If for any reason the government doesn’t inflate or merely doesn’t inflate as fast as required to support asset prices, there will be a massive bust. Most likely temporary, but possibly “permanent” if a new regime is anti-deficit.

Inflation is not a linear event either, but an exponential one. An economy living on credit needs an ever rising growth rate in credit to repay the existing credit that it cannot hope to repay except through new borrowing.

Financial asset demand is also the inverse of the rest of the economy. As financial asset prices rise, demand increases. A great example is homes. People want to buy cheaper homes, not more expensive homes because they are bought to live in. What happens in a speculative bubble? People chase and bid up home prices where they are rising the fastest. Price detaches from rents.

Layered on top of an unsustainable, exponential growth in money is financial speculation chasing the most unsustainable price increases. The exponent on the exponent.

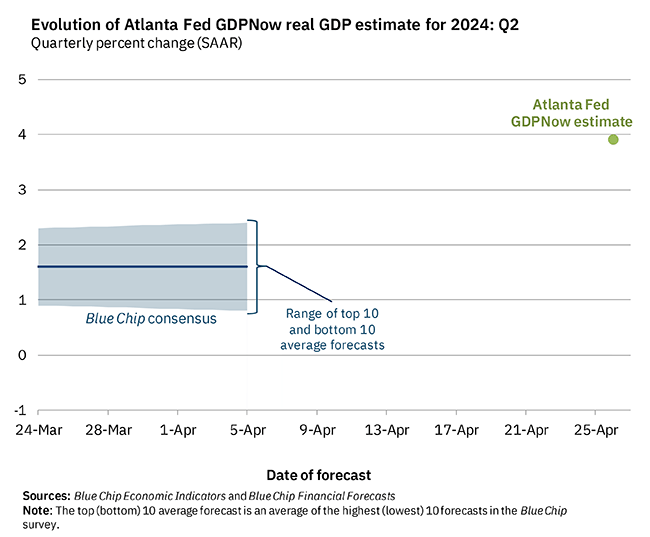

The Atlanta Fed’s GDP Now model put out its first forecast for Q2 GDP growth:

Events will be coming to a head soon.

Update: In early February, the model was +4.2 percent. The +3.9 percent above assumes +2.7 percent in consumer spending and net exports swinging from -0.86 percent to -0.05 percent.

Thank you!